Best Apps to Send Money to India from Estonia in 2026

Sending money from Estonia to India should be simple and cost-efficient, especially in a country known for its digital-first infrastructure. Yet many NRIs still end up paying hidden fees through poor exchange rates and outdated bank transfers. The difference between the right app and the wrong one can mean thousands of rupees lost every year without even noticing.

The top apps for EUR to INR transfers from Estonia are ZoltMoney (zero fees, real market rate), Wise (headquartered in Tallinn with transparent pricing), and Remitly (strong first-transfer offers and cash pickup options).

Here is how they compare against other popular options available today.

Why Estonian NRIs Often Pay More Than They Should

Estonia is one of Europe’s most digitally advanced countries, with e-residency, digital IDs, and a fully paperless ecosystem. Yet many NRIs in cities like Tallinn and Tartu still end up losing 2–4% on every transfer to India by relying on traditional banks.

A typical SWIFT transfer from banks such as Swedbank, SEB, or LHV costs €10–€25 in upfront fees. On top of that, banks apply a 1.5–3% exchange rate markup. This means the EUR to INR rate you see on your bank is lower than the real market rate shown on platforms like Google. The difference goes directly to the bank, reducing the amount your recipient receives.

Estonia’s strong fintech environment makes switching to better alternatives much easier. Wise was built in Tallinn and is widely trusted for its transparency.

ZoltMoney offers a stablecoin-powered transfer model that aligns well with Estonia’s digital-first mindset. With these modern options available, there is little reason to continue paying high bank fees for transfers to India.

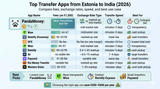

Top 7 Apps to Send Money from Estonia to India

Choosing the right app to send money from Estonia to India depends on your transfer size, urgency, and cost sensitivity. While several options are available, the real difference lies in fees, exchange rates, and how much your recipient actually receives.

Here is a breakdown of the most popular apps and how they compare in real-world usage.

ZoltMoney

ZoltMoney offers one of the lowest-cost ways to send money from Estonia to India. It provides zero transfer fees and uses the real mid-market EUR to INR exchange rate.

The platform runs on stablecoin infrastructure, which bypasses SWIFT and avoids intermediary bank deductions. This helps reduce both cost and transfer time.

For regular monthly transfers, this model ensures your recipient receives the full value of what you send.

Wise

Wise is headquartered in Tallinn and is widely trusted among Estonian users. It uses the real mid-market rate and charges a transparent fee of around €4–€7 per €1,000.

Transfers are fast and typically completed within 1–2 days. The multi-currency account is useful for users managing funds across different countries.

While reliable, the fee means it is not always the cheapest option.

Remitly

Remitly is a strong option for flexibility and speed. Its first transfer promotion can offer very competitive rates.

After the first transfer, exchange rates include a 0.4–1.4% markup. It supports multiple delivery options, including bank transfers, UPI, and cash pickup.

It is best suited for users who need flexible delivery rather than the lowest cost.

Xe

Xe works well for larger one-time transfers. It offers rate alerts that help users time the market.

However, the platform builds its margin into the exchange rate, which increases the overall cost compared to mid-market providers.

Paysend

Paysend is a simple option for small transfers. It charges a flat €1.50 fee, making it cost-effective for low-value transactions.

It is best used for quick transfers where convenience matters more than exchange rate precision.

Ria is mainly used for cash pickup. It has a wide network across India, making it useful for recipients without bank accounts.

However, exchange rates include a markup, which increases the total cost.

Western Union

Western Union is one of the most widely available services for cash pickup in India, especially in rural areas.

While reliable, it is typically one of the more expensive options due to higher fees and exchange rate margins.

Choosing the Right App Based on Your Transfer Needs

Monthly sender (€500–€2,000): ZoltMoney. The zero-fee, mid-market-rate model ensures you get the highest INR over time, especially for recurring transfers. Wise is the next best option if you prefer a well-established platform with transparent pricing.

Large one-off (€5,000+): Compare ZoltMoney and Wise before sending. Both use mid-market rates, so the key difference comes down to fees and timing. Checking rates on the day of transfer can help you maximise value.

Recipient needs cash: Remitly. It supports cash pickup across India, making it ideal if your recipient does not use a bank account. ZoltMoney and Wise are better suited for direct bank transfers.

Small transfers (€50–€200): Paysend. The flat €1.50 fee keeps costs predictable and low for smaller amounts. Wise’s percentage-based fee can feel expensive at this range.

Urgent transfers: Remitly Express. It offers near-instant delivery, which is useful for emergencies, though it may come at a slightly higher cost compared to standard transfers.

Knowing what drives EUR/INR rate fluctuations helps you decide whether to send now or wait.

Hidden Fees You Should Know Before Sending Money

Understanding the hidden costs behind money transfers is essential, as small fees and exchange rate differences can significantly reduce the amount your recipient receives over time.

FX markup disguised as zero fees

Many apps advertise zero transfer fees, but the real cost is often hidden in the exchange rate. If the EUR to INR rate offered is 1–2% worse than the mid-market rate you see on Google, that difference is effectively the fee. Over time, this can significantly reduce the amount your recipient receives. Platforms like ZoltMoney and Wise use the real mid-market rate, while many others build their margin directly into the exchange rate.

SEPA funding vs card payments

Funding your transfer through SEPA is usually free across all major Estonian banks such as Swedbank, SEB, LHV, and Coop Pank. In contrast, paying with a debit or credit card often adds an extra 0.5–2% cost on most platforms. This may seem small, but it adds up over regular transfers. Choosing SEPA funding is one of the simplest ways to reduce unnecessary costs.

Intermediary bank deductions on SWIFT

Traditional SWIFT transfers from Estonia to India often pass through intermediary banks, typically in financial hubs like London or Frankfurt. Each intermediary can deduct €10–€25, which means your recipient may receive less than the original amount sent. App-based transfers avoid this issue by sending money directly through Indian payment systems such as IMPS or NEFT, ensuring more of your money reaches its destination.

For a detailed comparison of how ZoltMoney stacks up against Aspora for EU corridor transfers, check the breakdown.

Example of Sending €1,000 from Estonia to India

To understand the real impact of fees and exchange rates, let’s look at a €1,000 transfer from Estonia to India. Even small differences in pricing can lead to noticeable changes in how much your recipient actually receives.

Assuming a mid-market EUR to INR rate of 95.00:

| App | Fee | Effective Rate | Recipient Gets (₹) |

|---|---|---|---|

| ZoltMoney | €0 | 95.00 | ₹95,000 |

| Wise | €5.50 | 95.00 | ₹94,478 |

| Remitly (regular) | €2.00 | 93.70 | ₹93,514 |

| Estonian bank wire | €20 | 93.00 | ₹91,140 |

As the comparison shows, choosing the right provider can make a meaningful difference. ZoltMoney delivers about ₹3,860 more than a traditional bank wire on a single transfer.

If you send money every month, this adds up quickly. Over 12 transfers, that is ₹46,320 extra reaching your family instead of being lost to fees and hidden markups.

Whether you are managing transfers alongside the cost of living as an NRI in Europe, or building a savings plan around remittances, that number adds up fast.

FAQs About Sending Money from Estonia to India

What is the cheapest way to send money from Estonia to India?

ZoltMoney currently offers the lowest total cost, with zero transfer fees and the real mid-market EUR to INR rate through stablecoin-powered infrastructure. Wise, which is also headquartered in Tallinn, is another cost-effective option with transparent fees of around €4–€7 per €1,000.

How long does a transfer from Estonia to India take?

App-based transfers such as ZoltMoney and Wise usually arrive within minutes to 24 hours. Remitly Express is faster for urgent transfers but often comes with a less favorable exchange rate. Remitly Economy can take up to 5 business days. Traditional SWIFT transfers from Estonian banks usually take 2–5 business days and tend to cost more.

Do I need an Estonian ID card to send money to India?

Most transfer apps require a valid government-issued photo ID, such as a passport, Estonian ID card, or EU residence permit. An Estonian ID card can be especially convenient because many services support eID verification. You will also need your recipient’s Indian bank account number and IFSC code.

Can I use my e-residency to send money from Estonia to India?

Estonian e-residency gives you a digital identity, but it does not automatically qualify you to use consumer money transfer apps from Estonia. Most platforms require proof of physical residence in an EU country along with local banking details. If you are living in Estonia with a valid residence permit, you can typically use these apps without issue. If you are an e-resident living elsewhere, you should use the app from your country of actual residence.

Are there any EU regulations on sending money from Estonia to India?

Yes, standard EU anti-money laundering rules apply to these transfers. While there is usually no hard cap on digital transfers, larger amounts may require additional KYC verification. Licensed services such as ZoltMoney, Wise, and Remitly handle these checks as part of their normal compliance process. On the Indian side, the RBI allows inward remittances under FEMA guidelines.

This blog is for informational purposes only and does not constitute legal, financial, or tax advice. Regulations, fees, and exchange rates change frequently. Consult a qualified CA or tax advisor for guidance specific to your situation.

Related Articles

Send Money to India

Send Money to Vietnam

Send Money to Philippines

Convert to Indian Rupee

Convert to Vietnamese Dong

Convert to Philippine Peso

Currencies

Send money to India, Vietnam, and the Philippines at real Zolt FX rates with zero hidden fees.

Company

Follow Us

Download App

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by ZoltMoney.

For any queries or grievances, please write to us at compliance@zoltmoney.com

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2026 ZoltMoney. All Rights Reserved.

Send Money to India

Send Money to Vietnam

Send Money to Philippines

Convert to Indian Rupee

Convert to Vietnamese Dong

Convert to Philippine Peso

Currencies

Send money to India and Vietnam at real Zolt FX rates with zero hidden fees.

Company

Follow Us

Download App

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by ZoltMoney.

For any queries or grievances, please write to us at

compliance@zoltmoney.com

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2026 ZoltMoney. All Rights Reserved.